Retirement Planning – SIMPLE IRA

Our Uncommon approach to personal finance does not mean you should ignore the more traditional methods of saving for retirement. There is a place for that in your portfolio.

Our Uncommon approach to personal finance does not mean you should ignore the more traditional methods of saving for retirement. There is a place for that in your portfolio.

And if you are a business owner, you’ll want to provide your employees with incentives like retirement savings as part of the standard compensation package. One of the most common places to invest retirement dollars is the Individual Retirement Account – the IRA.

The thing to know is that IRAs are not one-size-fits-all. We’ll be exploring various IRA vehicles, but for now, I want to walk you through the SIMPLE IRA. We love it for the small business owner because it is just as advertised – simple.

Here’s how the IRS describes them: “A SIMPLE IRA plan (Savings Incentive Match Plan) allows employees and employers to contribute to traditional IRAs set up for employees. It is ideally suited as a start-up retirement savings plan for small employers not currently sponsoring a retirement plan.”

How is a SIMPLE IRA Structured?

There are employee contribution guidelines and employer contribution guidelines.

Salary Reduction Contributions

These are taken out of the paycheck before taxes and put into the IRA. In 2020-2021, the maximum contribution is $13,000. But say you have other retirement programs. Can an employee put money into those as well? Yes, but total employee salary reduction contributions are capped at $19,500 for 2020-2021.

Employer Matching Contributions

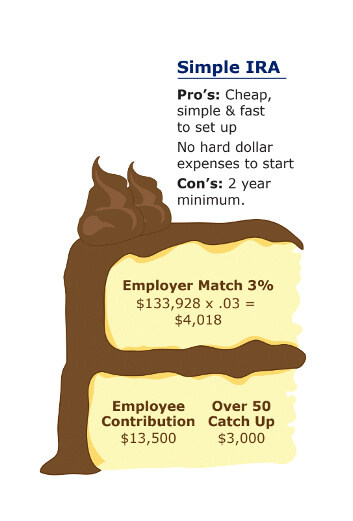

The SIMPLE IRA is meant for businesses with 100 or fewer employees. How does the employer match work with a SIMPLE IRA? The requirements from the IRS are that employee contributions be matched up to 3% of employee’s compensation.

As an employer, you have a few options for matching contributions. You can choose to do a 3% match as the standard contribution. Or you can contribute a percentage between 1 and 3% in no more than two out of five years. The other three years must be a match of the full 3%.

Non-Elective Contributions

The other option employers have is to make a non-elective contribution of 2% of eligible employee’s compensation. In choosing this option, employers make the 2% contribution whether or not employees make the salary reduction contributions.

If the employer chooses this 2% contribution formula, it must notify the employees within a reasonable period before the 60-day election period for the calendar year.

Eligibility

Employees who have worked for you for at least two years, earning at least $5,000 per year qualify for the SIMPLE IRA. Employees may NOT technically opt-out of the plan, but they may choose how little or how much, up to the limits, they take out of their pay. If the employee does not make salary reduction contributions, the employer would not have matching contributions to make. But if the employer chooses non-elective contributions, those would need to be made as for any other eligible employee.

Time limits for contributing funds

Employers are responsible to deposit employee’s salary reduction contributions no later than 30 days after the end of the month when the employee would have gotten that money as part of their paycheck

The due date for matching contributions or non-elective contributions is when the federal income tax return is due for that year.

Pros and Cons

What is nice about the SIMPLE IRA from an employer standpoint is that there are no fees or other monetary expenses to set them up. They really are simple. For you as the employer, be aware that matching contributions will need to be made in good years and bad years.

There are good reasons for you to set up SIMPLE IRAs for your employees. Be looking for upcoming articles on SEP and Roth IRAs for a full picture of how these work and which one might be right for you.

If you’d like to schedule a call for some help weighing the pros and cons, you can schedule a time here.